Got questions? Send us an email:

info@hpbs.uz

What is CBAM?

Carbon Border Adjustment Mechanism (CBAM), or the Carbon Border Adjustment Mechanism, is an initiative by the European Union (EU) that has garnered significant global interest and attention. Russian companies are also closely monitoring the EU's climate regulatory framework, as it is part of the global economy in which Russian organizations are embedded.

CBAM is a mechanism developed by the EU to combat climate change and reduce greenhouse gas emissions by economically offsetting so-called "carbon leakages" that occur when the EU imports carbon-intensive products from countries with underdeveloped carbon regulation. This mechanism involves imposing carbon taxes on imported goods (i.e., products produced with high greenhouse gas emissions will be taxed upon import into the EU). CBAM can be compared to a customs duty on imported products based on the amount of direct greenhouse gas emissions generated during their production.

What products are covered by CBAM?

Currently, six categories of products fall under mandatory CBAM regulation:

- Cement

- Iron and steel

- Aluminum

- Fertilizers

- Electricity

- Hydrogen

These categories are chosen because they are the most carbon-intensive, meaning they have significant greenhouse gas emissions during production. The movement of carbon-intensive products between countries causes inter-country "carbon leakages." Preventing these "leakages" is the primary goal of implementing CBAM in the EU.

"Carbon leakages" refer to greenhouse gas emissions that occur when products are manufactured outside the EU in countries with less stringent carbon regulation. Leakages occur when manufacturers move their production from countries with strict carbon emission reduction measures to regions with less developed or absent measures. As a result, such production does not fall under the regulatory framework for reducing greenhouse gas emissions and reporting. Consequently, the overall greenhouse gas emissions in the supply chain do not decrease, as production facilities outside the EU lack incentives to pursue low-carbon development. Additionally, imported products not taxed for carbon emissions lower the competitiveness of EU manufacturers' products.

Thus, the implementation of CBAM will increase the competitiveness of the EU's domestic products, prevent carbon leakages, and motivate manufacturers to reduce greenhouse gas emissions during production.

How is the CBAM tax determined?

The tax directly depends on the number of greenhouse gas emissions associated with the production of imported products. The calculation considers direct emissions under Scope 1 related to the production technology of goods and, during the transition period, indirect emissions from purchased energy used in production.

How is the tax paid?

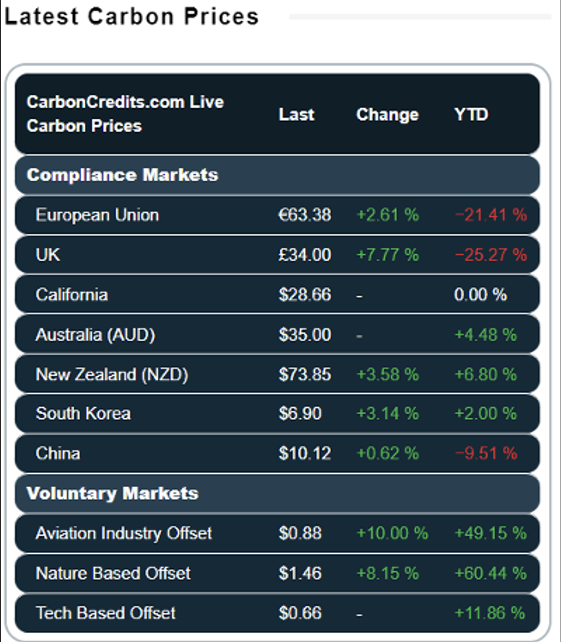

CBAM requires the purchase of so-called CBAM certificates on the EU ETS (Emissions Trading System) exchange to pay for emissions. One certificate will cover emissions of one ton of CO2e. The certificate's cost will equal the price of a carbon unit on the EU ETS exchange. For example, as of January 31, 2024, the cost of one CBAM certificate would be €63.38 (according to the information platform https://carboncredits.com/).

When determining the amount for which carbon certificates must be purchased, payments for exceeding CO2e quotas or acquired carbon units in the product's country of origin can be considered. Therefore, if a manufacturer can prove that they have already paid for exceeding CO2e emissions under the carbon regulation of the state where the production is located, the corresponding amount of emissions can be deducted from the tax amount (this procedure is stipulated in Article 7 of EU Commission Regulation 2023/1773). In this case, importers will need to purchase certificates only for the difference between the calculated CBAM emissions and the emissions already paid for before importing the product into the EU.

For example, in the Russian Federation, part of the embedded emissions under Scope 1 can be "offset" by accounting for the mandatory quota under Federal Law No. 296 "On Limiting Greenhouse Gas Emissions" (currently, payments for exceeding emission quotas exist for the Sakhalin region).

When does CBAM come into effect?

The full requirements of CBAM will come into effect on January 1, 2026. From this date, manufacturers must calculate greenhouse gas emissions during product production, declare the quantity of goods imported into the EU, and pay taxes by purchasing the appropriate number of CBAM certificates.

However, starting October 1, 2023, a transition period for CBAM implementation began, regulated by EU Commission Regulation 2023/1773. During this period, importers are required to submit quarterly reports containing the following information:

- The total quantity of each type of imported goods included in the CBAM list (in MWh for electricity or in tons for other goods);

- The actual embedded emissions of the products, considering direct emissions during production (in tons of CO2e/MWh for electricity or in tons of CO2e/ton for other goods). Embedded emissions in CBAM methodology refer to the specific carbon footprint of the product, i.e., the amount of carbon released during product creation;

- Total indirect emissions (including the amount of consumed electricity and applicable emission factors);

- The carbon price embedded in the emissions in the product's country of origin if carbon taxation has already been applied to the imported goods.

The first quarterly report for the transition period was due by January 31, 2024. Additions and corrections to the submitted report can be made until July 31, 2024. This allows declarants to adapt more flexibly to new emission calculation methodologies and reporting requirements.

Starting January 1, 2026, importers must register as authorized declarants and begin purchasing CBAM certificates for imported CO2e emissions. During this period, mandatory annual emission declarations (i.e., annual CBAM declarations) will be introduced, including specific data such as verified calculations of the embedded carbon footprint.

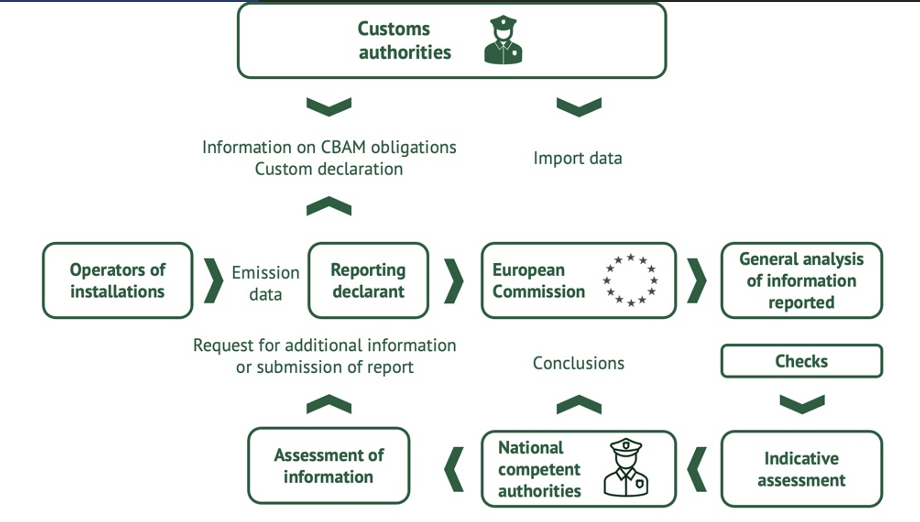

CBAM Import Procedure

Carbon Footprint Calculation Manufacturers of goods imported into the EU are advised to calculate the carbon footprint of their products. Each product type subject to CBAM requirements has its methodologies for calculating greenhouse gas emissions. For simplification, an online calculator is available on the EU website, which is currently being refined. The calculated embedded emissions values are provided by manufacturers to EU product importers.

Registration in the CBAM Registry Importers who submit customs declarations must register in the CBAM authorized declarant registry.

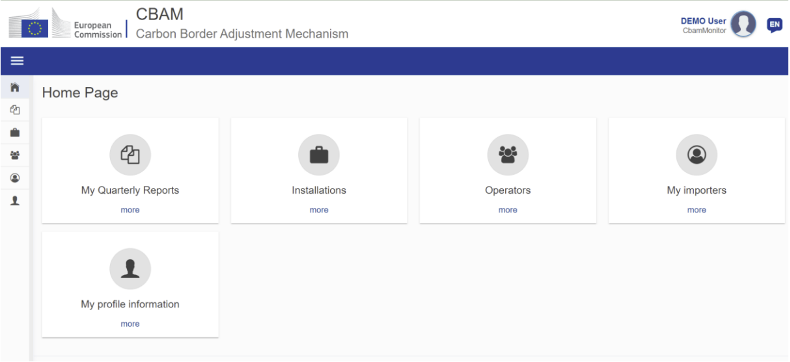

Submitting CBAM Reports A compiled report containing information on purchased product volumes, direct and indirect emissions, embedded product emissions, and other required information is submitted for review via the CBAM Reporting Declarant Portal (https://cbam.ec.europa.eu/declarant).

Photo: https://cbam.ec.europa.eu/declarant

Audit and Verification The results of the carbon footprint calculation may be audited and verified to ensure the accuracy and reliability of the information provided.

Determining the Tax Rate Based on the carbon footprint calculations, a tax rate for specific products is determined. The tax rate calculation considers emission payments that the manufacturer has paid in the production region according to local carbon regulations.

Tax Collection The established tax is paid by purchasing and providing a specific number of CBAM certificates by product importers. Certificates will be purchased on the EU ETS, and their cost will equal the carbon unit price on the EU ETS exchange. The specific mechanisms for purchasing certificates are not yet established and will be developed during the transition period of the CBAM system implementation.

Continuous Improvement of CBAM

The CBAM system will be continually refined during its implementation. The list of products subject to CBAM requirements, as well as the emission categories that need to be accounted for, will be expanded. By 2034, it is planned that 100% of embedded emissions of imported products will be taxed. Therefore, it is strategically important for all companies supplying products to the EU to calculate and declare greenhouse gas emissions following CBAM requirements.

Authors: Marina Kupriyanova